{kind=link}

This report is the first in a series on “Europe’s energy transition: Balancing the trilemma” produced by the Brookings Institution in partnership with the Fundação Francisco Manuel dos Santos.

Providing a stable energy supply is often described in terms of a “trilemma”—a balance between supply security, environmental sustainability, and affordability. Of the three pillars of energy supply, security is the easiest to take for granted. Supply seems fine until it isn’t. Security of fossil fuel supply is particularly easy to ignore in countries that are striving to greatly reduce their fossil fuel consumption for climate reasons. The political focus is on building renewable energy and zero-carbon systems, and mitigating the economic, social, and political costs of transition; the thought was that the existing system would take care of itself until it was phased out. This was the case for much of Europe until two years ago.

Russia’s full-scale invasion of Ukraine on February 24, 2022, shocked Europeans into realizing that they could no longer take the security of their fossil fuel supply for granted. The assumption had been that Europe and Russia were locked into a mutually beneficial, secure relationship, since Europe needed gas and Russia had no infrastructure to sell that gas anywhere else. That belief turned out to be wrong.

When the war began, Europe was importing a variety of energy products from Russia, including crude oil and oil products, uranium products, coal, and liquefied natural gas (LNG). But the Kremlin’s sharpest energy weapon was natural gas, delivered by the state-backed gas monopolist Gazprom via pipelines and based on long-term contracts. Europe needs gas for power generation, household heating, and industrial processes.

Before the invasion, more than 40% of Europe’s imported natural gas came from Russia, its single largest supplier, delivered via four main pipelines. Some European countries relied on Russia for more than 80% of their gas supply, including Austria and Latvia. But Germany was by far Russia’s largest gas customer by volume, importing nearly twice the volume of Italy, the next largest customer. “Oil and gas combined account for 60% of primary energy,” wrote the Economist in May 2022, “and Russia has long been the biggest supply of both. On the eve of the war in Ukraine, it provided a third of Germany’s oil, around half its coal imports, and more than half its gas.”

Figure 1

Gas flows to Europe

This paper launches a project on European energy security in turbulent times by analyzing the European response to drastically reduced supplies of Russian pipeline gas. Future papers in the series will delve more deeply into specific aspects of European energy security and their policy implications.

Russia’s actions to cut off gas supply to Europe starting in May 2022 were particularly virulent because it was extremely difficult to cope with the loss of such a large volume of gas. Other regional sources of pipeline gas (e.g., from the North Sea) have been declining and key sectors of European industry (e.g., chemicals) depend on gas as their primary energy source. LNG is a potential substitute for pipeline gas, but it requires specialized infrastructure and global LNG markets were already tight, with much of the world’s supply going to Asia.

The story of Europe’s adjustment to its main supplier of natural gas turning off the taps is generally told in heroic terms: with the continent securing new supply, conserving or substituting (often with generous government subsidies for industry and/or consumers) in order to weather the storm, and throwing Russia’s weaponization of gas back in its face through declining revenues. This narrative is not false, and the scale and speed of the response would certainly have been politically unimaginable before the invasion. But the self-congratulatory tale masks the fact that there were substantial regional differences in both energy supply and response to the crisis, which will make it difficult to generate a Europe-wide political response in the future.

Even more importantly, the decoupling is by no means complete. Overall, in 2023, Europe still imported 14.8% of its total gas supply from Russia, with 8.7% arriving via pipelines (25.1 billion cubic meters or bcm) and 6.1% as LNG (17.8 bcm). (For comparison, during the first quarter of 2021, 47% of Europe’s total gas supply came from Russia, 43% via pipeline and 4% as LNG.)This means that the handful of member states that have not been able to or have not chosen to reduce their dependency remain highly vulnerable to Russia’s weaponization of energy imports.

How Russia engineered its grip on Europe’s gas supply

Russia has a long history of using its dominance in pipeline gas supply to Europe for political ends, especially related to the Russian gas pipelines that run through Ukraine. In 2006 and 2009, disputes with Ukraine over the terms of transit contracts led to cutoffs of Russian gas supply, affecting many countries in the region. Less dramatic disputes occurred between Russia and Poland over transit to Europe through the Yamal pipeline. (Ronald Reagan opposed the construction of the Yamal pipeline in the 1980s, concerned about the leverage it would give the Soviets over Europe. His concerns were prescient.)

More recent Russian pipeline projects, including the TurkStream and Nord Stream projects, were intended to circumvent the need to ship gas through Ukraine and avoid paying transit fees to its government. The recipient countries of these pipelines were usually happy to have a more direct connection to Russian gas supply, not subject to disputes between Russia and Ukraine. At the same time, these pipelines were clearly also intended to deepen mutual political ties.

Russia’s involvement in the German gas sector is the most notable case in point. The Nord Stream pipeline provides a direct connection from Russia to Germany beneath the Baltic Sea, avoiding any transit via Ukraine, Poland, Belarus, or the Baltic states. The venture was a project of Russian President Vladimir Putin with his friend German Chancellor Gerhard Schröder, who signed a joint declaration of intent for the project in early September 2005, just before losing national elections against Angela Merkel. Immediately after stepping down, Schröder joined the new pipeline consortium’s board.

The first Nord Stream pipeline, also known as Nord Stream 1, is a joint venture with a 51% share held by Russia’s Gazprom and the other 49% held by a group of European companies. (It consists of two physical pipes, NS 1 A and B, one of which began operation in November 2011 and the other in October 2012.) With a capacity of 55 bcm per year, Nord Stream became the largest source of Russian gas supply to Europe; it supplied two-thirds of Germany’s total imports in 2021. Gazprom’s involvement in German and regional gas markets deepened when it bought a quarter of Germany’s underground gas storage facilities, including the largest such facility in Western Europe, at Rehden, from their German owner, BASF. The deal initially broke down after Russia’s illegal annexation of Crimea in February 2014, but finally went through in 2015.

The Nord Stream 2 project was announced in 2015 with significant controversy. The argument centered on whether it was a commercial project, intended to meet Europe’s growing demand for natural gas, or a geopolitical project intended to deepen Russia’s dominance of European gas markets and to starve the Ukrainian economy of revenues from natural gas transit. The United States opposed the pipeline, along with Ukraine and many Eastern European nations, while German Chancellor Angela Merkel strongly supported it.

This second set of two pipelines (NS 2 A and B), which was to double Nord Stream 1’s capacity to a total of 110 bcm/year, was completed in September 2021 but never went into operation. Germany stopped the approval process for Nord Stream 2 on February 22, 2022, two days before Russia’s full-scale invasion of Ukraine, when Russia recognized the eastern Ukrainian “republics” of Luhansk and Donetsk, parts of which it had occupied since 2014. Subsequently, on September 26, three of the four pipes making up the Nord Stream system were severely damaged in what by all accounts was an act of sabotage. Despite much speculation and the opening of several government inquiries, the perpetrators have still not been identified. (Some of these inquiries have since been closed, without making a definite finding.)

Russia weaponizes energy—but Europe strikes back

Those who advocated long-term, exclusive pipeline gas contracts between Russia and Europe had depicted these relationships in the most glowing and mutually beneficial terms—almost like a marital union. A German member of the European Parliament summarized this widely-shared sentiment in 2018, saying, “The Russian economy is highly dependent on the income from gas exports to the EU, which creates a strong mutual dependence between us.” But as a husband, Russia proved to be the Bluebeard type. Putin has turned Europe’s natural gas market into another front in his country’s war against Ukraine, weaponizing Russia’s previous market dominance in order to coerce Europeans into acquiescence, or at least to paralyze them politically and thus prevent them from supporting Kyiv. That attempt has not just failed but led to a near-complete split—and as in most divorces, it has been painful for both sides.

In retrospect, it is clear that Russia began preparing gas cutoffs before the full-scale invasion. In 2021, a sharp economic rebound from a pandemic slump, strong demand for LNG in Asia, and a particularly cold winter and spring led to soaring natural gas prices in Europe and very low levels of gas storage heading into the winter. Russia began slowing supply to Europe that summer, providing contractually obligated volumes of gas, but not the extra spot sales that typically occurred, and not filling Russian-owned gas storage in Europe. Gazprom denied that it was restricting gas supplies, but the head of the International Energy Agency, Fatih Birol, countered that Moscow could increase supplies by a third if it chose. Putin responded by suggesting that Germany would need to certify the Nord Stream 2 pipeline.

The gas conflict came to a head in March and April of 2022, soon after Russia invaded Ukraine. Russia demanded that its European customers open accounts at Gazprombank and pay for their gas in rubles, instead of the euros or dollars stipulated in contracts. This was an effort to use these gas payments to prop up the ruble and keep Russia connected to the global banking system, after Western sanctions cut off Russia’s central bank and caused the ruble’s value to plummet.

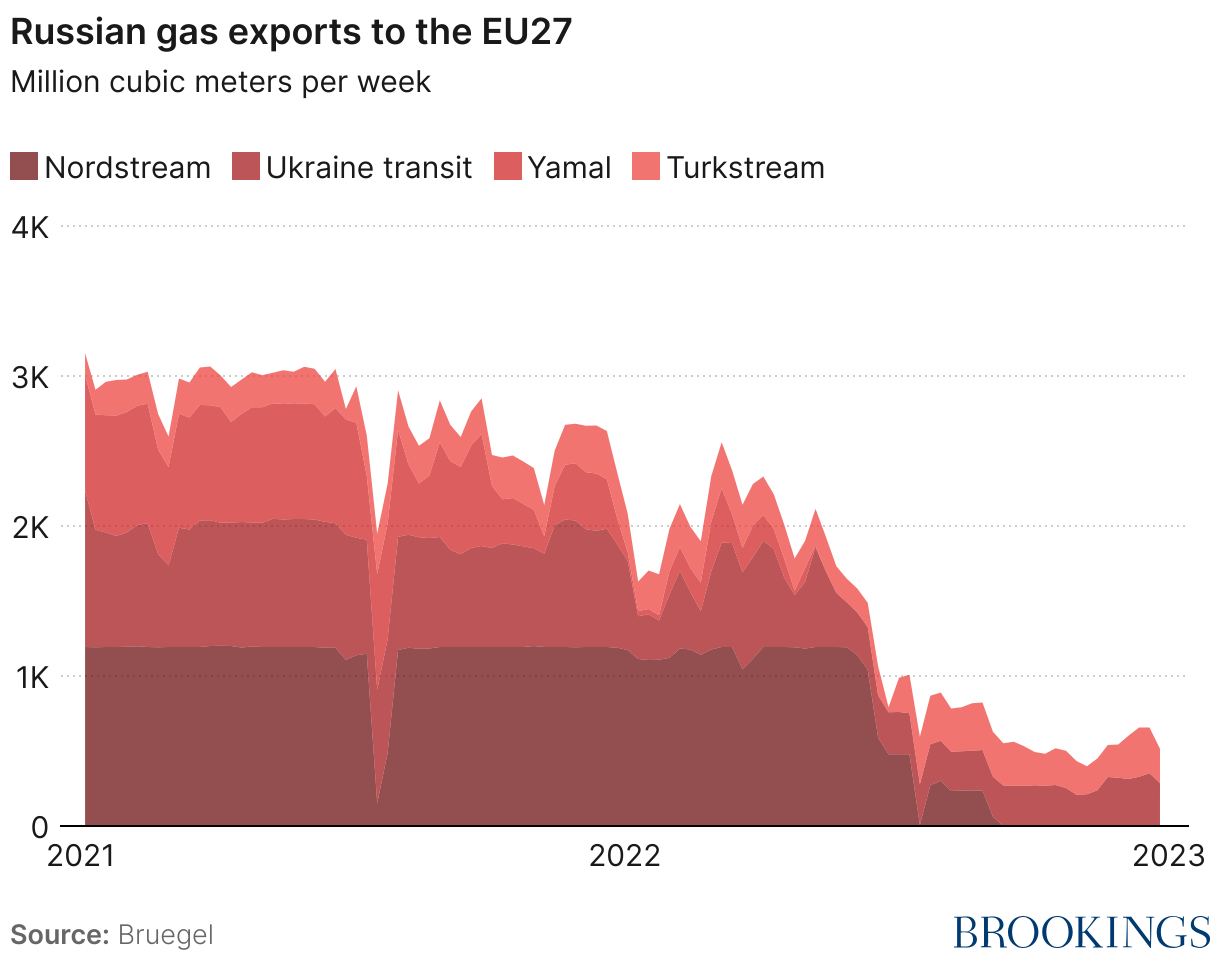

Cutoffs began in earnest in May 2022 after buyers refused to pay in rubles. Russia cut off the gas supply through the Yamal pipeline to Poland and the Gryazovets-Vyborg pipeline to Finland. Russia suspended the supply of gas indefinitely through Nord Stream 1 on September 2, 2022, after the G7 countries committed to imposing a price cap on Russian oil. An additional cut to supply occurred when Ukraine’s gas operator (Gas Transmission Systems Operator Ukraine, or GTSOU) cut off supply through the Sokhranivka transit point, located in the Russian-occupied Luhansk region. This route had previously carried about one-third of Russian gas supplied through Ukraine.

By late September, Russian supply was less than 20% of its previous level. Russia’s share in European gas supply declined to about 15% by the end of 2023. Some gas is still reaching Europe through Druzhba (Friendship), the main Ukrainian transit pipeline, and through the TurkStream pipeline, but the Nord Stream pipelines to Germany and the Yamal pipeline to Germany through Poland have ceased operation entirely.

Figure 3

Ukraine’s Western supporters, for their part, set about attempting to counter-weaponize their energy relationships with Russia in order to reduce the country’s revenues (energy sales made up 45% of government revenue in 2021) and to starve the Russian war machine. The results have been mostly mixed.

On December 5, 2022, the United States, the European Union, and several other countries set a price cap for Russian oil sales shipped using Western tankers or insurance services, which historically accounted for more than 90% of Russian sales. Given that Russia was the world’s second-largest oil exporter in 2021 after Saudi Arabia, removing Russian oil from the marketplace entirely would have risked destabilizing the global economy with very high oil prices, and was thus infeasible. The price cap was a novel policy which set the price for Russian crude oil at a level above production costs, but below benchmark prices on world markets—thereby providing a mechanism for Russian oil to be sold while reducing Moscow’s revenues. The assumption was that Russia, in order to maintain its export earnings, would continue to export oil as long as the capped price exceeded the production cost.

In the early days of the cap, Russian oil traded below the price cap and at a discount to Brent crude (a type of crude oil that serves as a price benchmark) of more than $30 per barrel, oil tax revenues fell by more than 40%, and the volume of seaborne exports was stable. (The most common grade of Russian crude oil, Urals, is a lower-quality crude oil than the Brent benchmark; it generally sold at a slightly lower price than Brent even before the price cap.) In the summer of 2023, the discount on Russian oil narrowed as Russia switched to a “shadow fleet” of shipowners and insurers not bound by the cap. But in recent months, revenues are declining again, in part because of a decrease in refined product exports due to Ukrainian drone strikes on Russian refineries.

Oil is generally fungible and Russian oil is almost fully reaching the market, as the policy intends. Several countries, particularly India, have greatly increased their purchases of Russian crude oil at discounted prices, although increasing use of the shadow tanker fleet has reduced the effectiveness of the price cap over time. After an initial price spike, benchmark global oil prices are back to their pre-invasion range. The precise impact of the oil price cap is difficult to determine, as prices for Urals crude are not transparent, but data suggests that consistent enforcement of the cap is putting downward pressure on the prices Russia receives for its oil.

Figure 4

As for the European Union, energy policy is in its DNA, since it grew out of the European Coal and Steel Community that was established in 1951 to deal with energy supply issues arising out of World War II. But the subsequent history of the European Union’s (EU) energy policy is one of constant tension between national protectionism and the EU’s attempts to deepen integration and remove barriers to cross-border energy trade, to address climate and sustainability issues, and finally—following the Russian-Ukrainian gas disputes of the mid-2000s and the geopolitical tensions in Northern Africa and the Middle East—to achieve supply security. It was only in 2015 that the “Energy Union” framework tried to connect the EU’s climate and renewable energy goals and its energy security strategy under one roof.

Weeks after Russia’s invasion of Ukraine, the European Commission announced the REPowerEU plan to transition away from dependence on Russian fossil fuels by 2027. It followed with embargoes on coal (August 2022), crude oil imports (December 2022), and oil products (February 2023), and it participated in the G7 oil price cap.

But the EU has not sanctioned Russian gas supply (or for that matter nuclear fuel products), fearing that this might destabilize markets; three of its 27 member states—Hungary, Austria, and Slovakia—still do not have other sources of gas than Russian pipelines. Instead, in August 2022, the EU agreed on a voluntary 15% target for a reduction in gas demand across the continent through March 2023; this request was extended through March 2024 and once more until March 2025. It did not take into account countries’ differing uses of gas and the varying difficulty of replacing gas across sectors.

At the end of 2023, the EU reformed its gas market rules to allow individual countries to ban the delivery of Russian gas, through pipelines or as LNG; this could provide a basis for energy companies to invoke force majeure (the contract law principle which allows parties to terminate a contract in case of exceptional or catastrophic unforeseen events) to get out of long-term contracts with Russian providers. Still, Moscow’s LNG imports to the EU have actually increased; some is shipped on to third countries, but the rest stays in the EU. These sales generated an estimated €8.2 billion for 20 bcm in 2023, financing the Russian war effort. This is why the EU is now proposing limited restrictions on Russian LNG transiting the bloc to outside buyers—its first foray into gas sanctions; the Baltics and Poland reportedly even want a total ban.

In a Brookings paper on economic activity from September 2023, German economists Benjamin Moll, Moritz Schularick, and Georg Zachmann endorse gas sanctions and point out that as Europe will use natural gas for at least two more decades, “Europe should consider taking advantage of the historically low flows to establish joint political control over gas flows from Russia rather than buying cheaply produced gas at high prices.”

Just how far Europe has to go to fully forgo Russian gas was demonstrated by a recent news report that in May 2024, Russian gas imports to the EU overtook those from the United States, the bloc’s largest LNG supplier. In all likelihood, this is a temporary spike: U.S. LNG exports have been lower than normal after an outage at an important export facility; also, another factor to keep in Russian pipeline exports through Turkey have been higher than normal due to planned maintenance.

Nonetheless, Russia’s self-inflicted dilemma is acute. Fields that supplied Europe are not connected to other customers, nor to facilities that allow that gas to be liquified and sold as LNG; therefore the gas that would have been sold to Europe is staying in the ground. Although Russia would like to sell more gas to China, no pipeline connects these gas fields to China and China has shown little interest in a proposed pipeline connection. The fact that Gazprom’s financial results for 2022 were actually better than the previous year, despite steep declines in exports in the second half of the year, was because high prices made up for smaller volumes. But the Russian monopolist’s earnings in 2023 were 40% below their 2022 level; its gas exports were nearly cut in half; and it posted a net loss, of $6.8 billion, for the first time since 1999.

Geography is key to Europe’s gas security challenges

Natural gas is used quite differently from one European country to the next, for reasons including weather, industrial and household usage, and the availability and preferences for alternative forms of energy. For example, gas is important for heating homes in Northern Europe’s colder climates, while France’s vast investments in nuclear power mean that little natural gas is used in power generation there.

Some uses can be more easily substituted, such as moving from natural gas-fired power generation to renewable electricity or other forms of fossil fuel generation. Building new electricity generation capacity takes time, but electricity systems are often sufficiently diversified and have enough capacity that other forms of generation can substitute. However, in the near term, this often means running more coal-fired generation. Extending the lifetime of existing nuclear reactors is another option, as is currently happening in Belgium.

Other uses of natural gas are much more difficult to substitute. Electric heat pumps are a fine substitute for natural gas in home heating, but installing them in millions of individual homes and businesses is time-consuming, expensive, and requires the will and cooperation of building owners. When German economics minister Robert Habeck attempted in 2023 to force the adoption of heat pumps by law within a year, he set off a political storm (the law later passed with a longer timeframe and more exemptions). Additionally, many industries that use natural gas require combustion to achieve very high process heat. Natural gas is the cleanest fuel for these applications. Industries that use natural gas as a raw material, like the chemicals industry, find it especially difficult to substitute.

A combination of conservation and fuel switching helped Europe get through the winter of 2022-23 (along with the blessing of unusually warm weather). The winter of 2023-24 played out similarly, with gas added to storage later in the season than usual as warm weather continued into the fall. The same factor affected demand differently from one country to the next; for example, in the winter of 2022-23, about 20% of Germany’s gas demand reduction was driven by warmer weather, whereas in France the figure was 60%.

An additional factor that is buried by considering Europe as a whole is that sources of natural gas differ greatly across Europe. Although overall 40% of European gas imports came from Russia before the conflict, this statistic hides almost total dependence in some areas and little supply to others. Thus, the question became not just of replacing gas in general, but of finding mechanisms of moving gas to areas that were previously served by Russian pipelines.

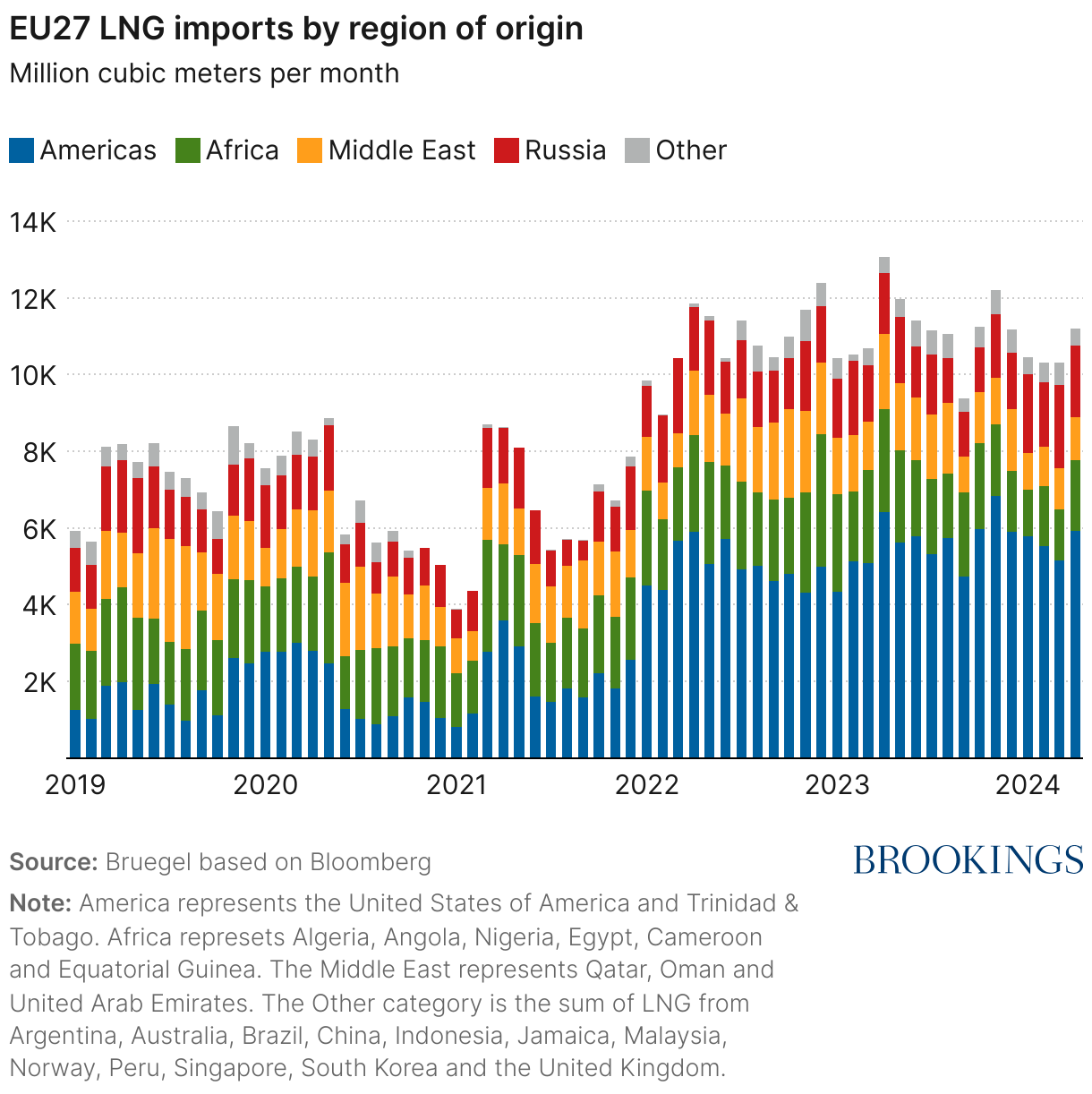

LNG has been a key mechanism to replace Russian pipeline gas, achieved especially through the deployment of floating regasification and storage units (FSRUs). These units receive LNG from transport vessels and transform it from liquid back to its gaseous state. Facilities to connect these vessels can be built much more quickly than a full onshore regasification facility, and Europe secured 12 new FSRUs in 2022. Since the beginning of the war in Ukraine, Europe has added 53.5 bcm of LNG import capacity, including expansion of a terminal in France and FSRUs in Finland, the Netherlands, Germany, and Italy. In 2022 and 2023, LNG made up 34% and 37% of Europe’s natural gas consumption, respectively, up from 19% in 2021.

The EU permitted exemptions from its rules limiting state aid for the construction of LNG facilities after the Ukraine war began. Germany passed the LNG Acceleration Act, simplifying and expediting the licensing of FSRU terminals, and in November 2022 fully nationalized Gazprom Germania, a wholly owned subsidiary of Gazprom that is now known as Securing Energy for Europe (SEFE).

Additionally, although areas served primarily by LNG before the conflict were less directly affected by the gas cutoff, they did experience much higher LNG prices as competition for gas increased. As a result, these countries also paid a price for the cutoff and had incentives to reduce demand as a result.

Figure 5

Continental transit hub: Germany

Before Russia’s full-scale invasion of Ukraine, Germany received about 65% of its gas supply from Russia and in turn supplied gas to other countries in Eastern Europe, including the Czech Republic, Austria, and Poland—it was and arguably remains the key gas transit hub in continental Europe. With the shutdown of the Nordstream and Yamal pipelines, Germany lost all its Russian pipeline supply in September 2022. The extreme reliance of Germany and its neighbors on Russian pipeline gas meant that actual physical shortages were a possibility after the cutoff, unlike in other areas where the primary concern was high prices.

Germany has largely swapped dependence on Russia for dependence on Norway for its pipeline gas supply. In December 2023, SEFE signed a new $55 billion long-term contract with the Norwegian producer Equinor. The contract calls for Equinor to supply 111 Terawatt-hours (TWh) of gas (or about 10 bcm) annually for the next 10 years, about 16% of the supply that Germany received through the Nordstream pipeline before the war. With this new contract, approximately 60% of Germany’s gas supply will come from Norway.

However, some of Germany’s neighbors remain dependent on Russian gas. For example, Austria’s dependence on Russia reached 98% at the end of 2023, its highest level since the war began. The partially state-owned company OMV has stated that it intends to keep buying gas from Gazprom under a contract that runs until 2040. The challenge is that ending the confidential long-term contract would likely trigger an early termination fee worth more than €1 billion. Policy support, such as a law requiring the end of Russian supply that might allow OMV to claim force majeure, would likely be needed for such a move.

The remainder of Germany’s gas needs are now met by LNG supplied by the United States, Qatar, and Russia. Before the crisis, Germany had no LNG import terminals, although it imported gas from other countries, particularly Belgium and the Netherlands, that originally arrived in Europe as LNG. After the cutoff of Russian supply, Germany implemented a crash program to add LNG import capacity with FSRUs, and the first of these receiving facilities completed construction in a record nine months. Three FSRUs are currently in operation, with two more set to come online in early 2024. Germany’s economy ministry has stated that it expects LNG import capacity to reach 37 bcm/year in 2024.

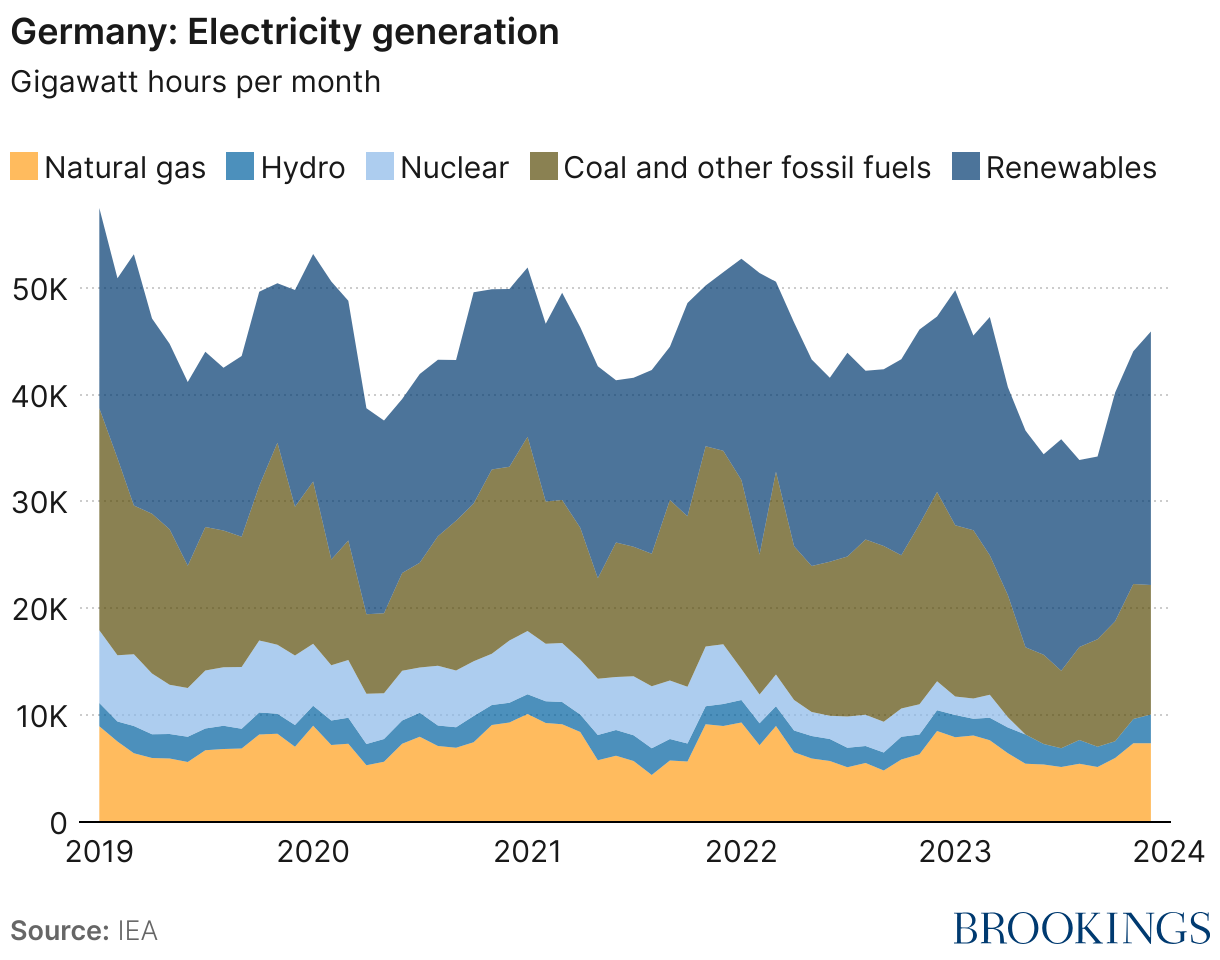

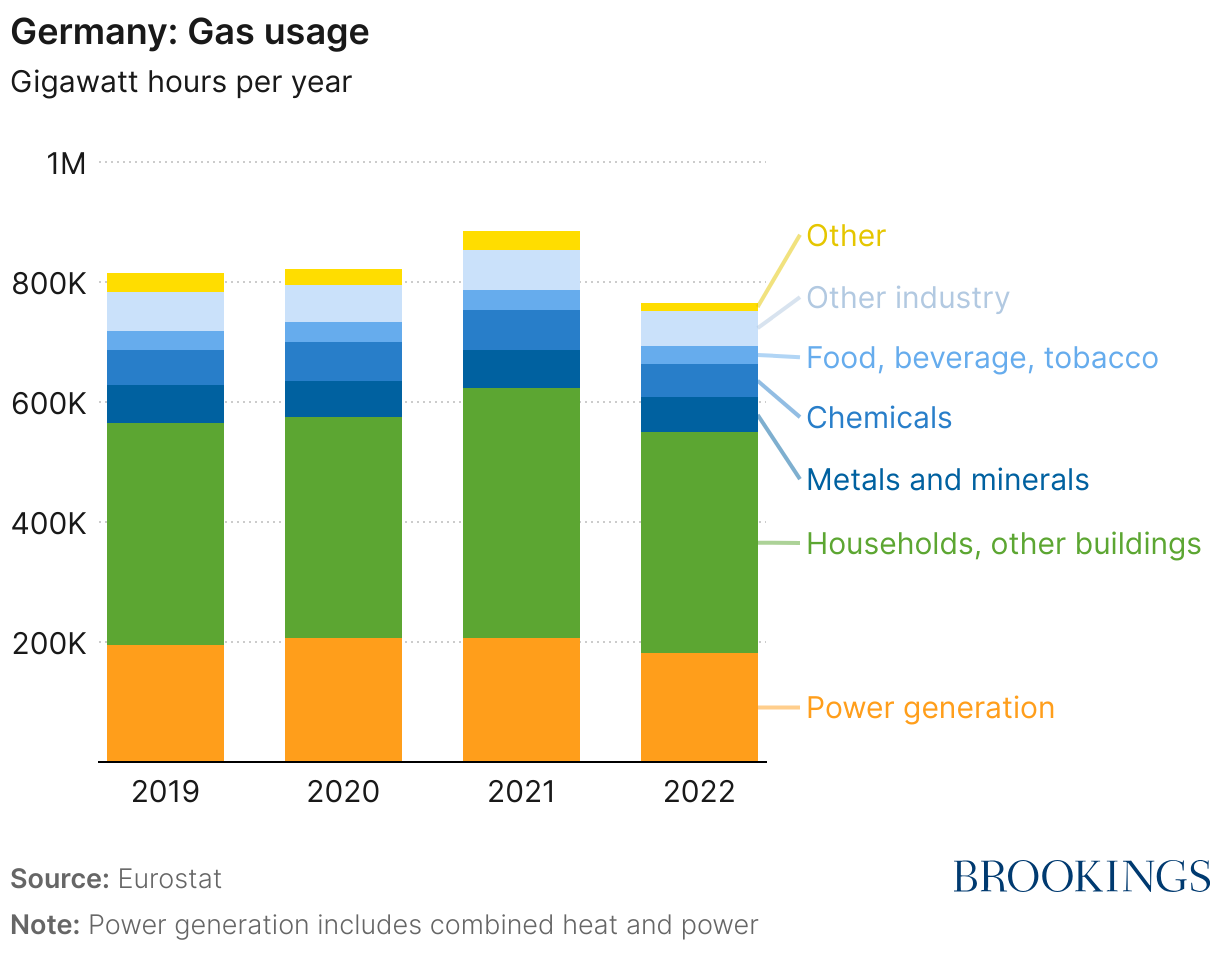

Increasing supply from other sources has been central to Germany’s crisis response. But demand reduction also was a key component of weathering the crisis. From July 2022 to March 2023, natural gas demand in Germany decreased by about 20%, with the largest contributions from industry with a 26% reduction, and households with a 17% reduction (with help from a mild winter). Reduction in industry use came mostly from energy-intensive sectors like chemicals, paper, or fertilizer, with significant drops in production and increases in imports. For example, BASF is closing an ammonia plant in Germany, stating that, “High energy prices are now putting an additional burden on profitability and competitiveness in Europe.”

However, German industrial substitution came with negative ecological side effects, since it often switched gas for fuel oil. And despite its strong anti-nuclear lobby, Germany briefly extended the life of its last three nuclear reactors and it brought several mothballed coal-fired plants back online. Finally, the German government’s sweeping up of LNG on world markets and its immense subsidy packages for industry and consumers limited supplies for other countries and drove up prices, angering poorer EU neighbors and EU officials in Brussels.

Figure 6

Figure 7

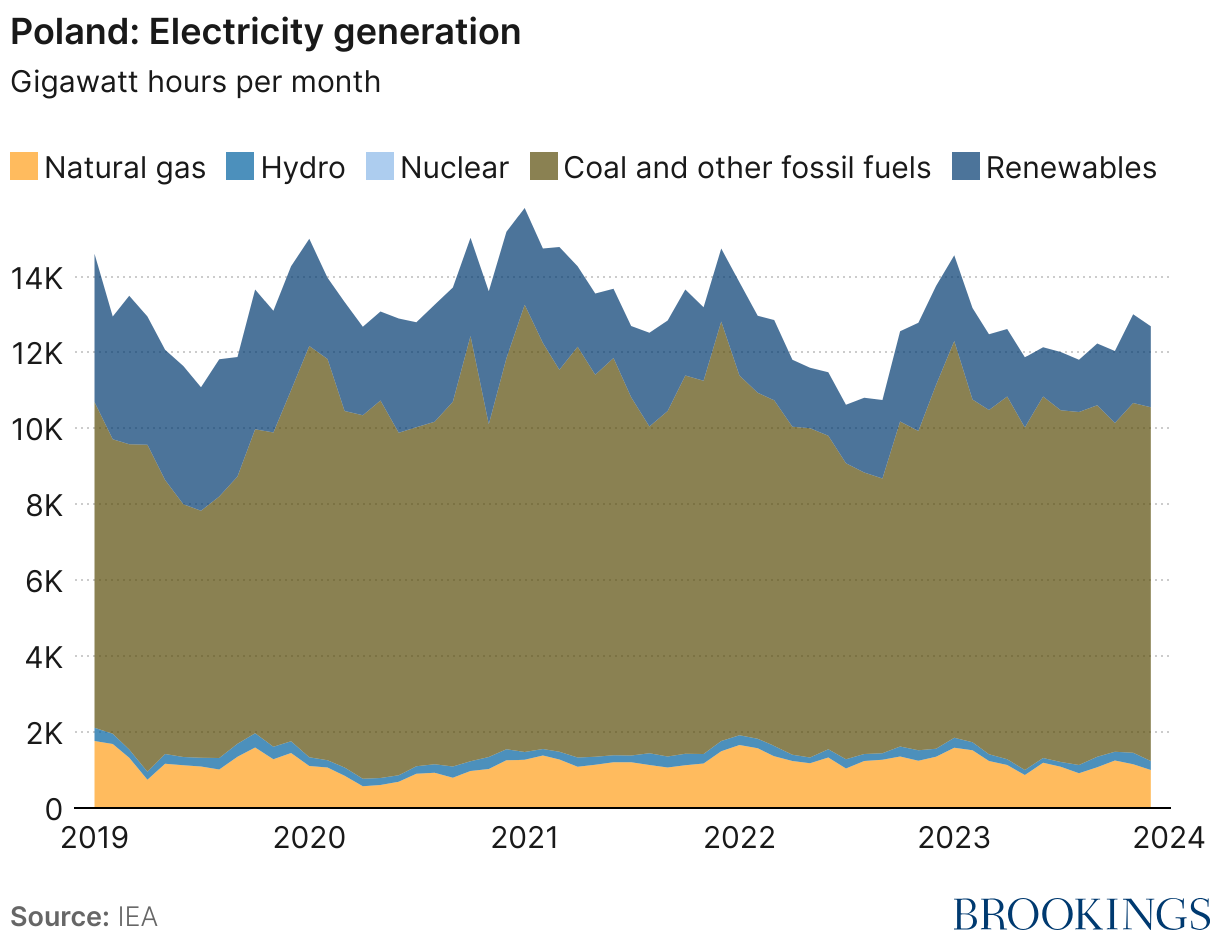

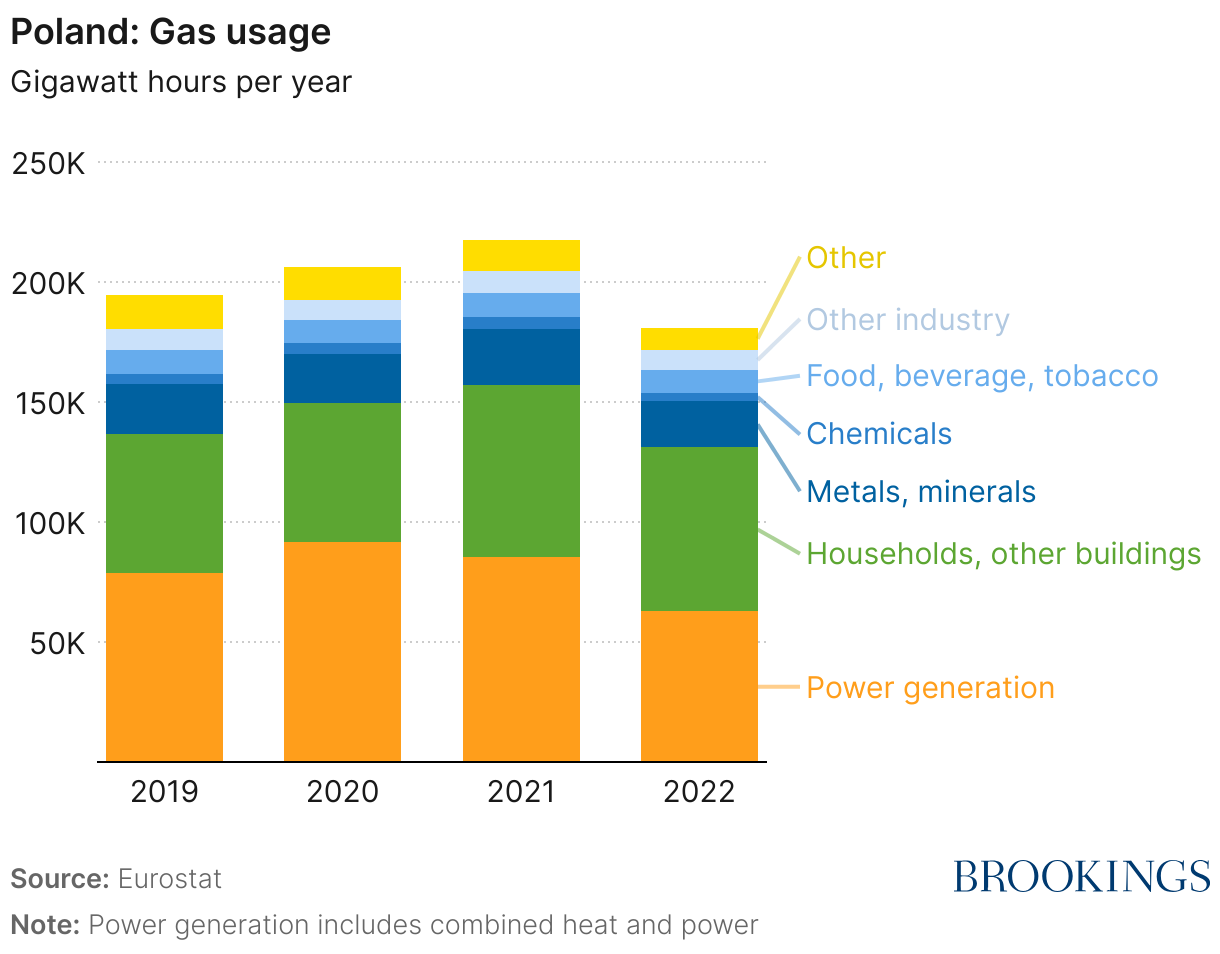

Northeastern connectors: Poland, Finland, Baltic states

Gazprom unilaterally cut gas supplies to Poland in April 2022, and to Finland and Latvia in August of that year; Estonia and Lithuania had stopped importing Russian gas in April.

The European Commission’s Baltic Energy Market Interconnection Plan aims to achieve open and integrated energy markets in the region. Participating member states are Denmark, Germany, Estonia, Latvia, Lithuania, Poland, Finland, and Sweden, with Norway participating as an observer. In addition to the work already done to integrate natural gas markets, Estonia, Latvia, and Lithuania are working to disconnect their electricity grid from Russia and Belarus and synchronize with the European grid. The planned deadline for this project was recently moved forward, from the end of 2025 to February of that year.

Infrastructure investments begun well before Russia invaded Ukraine have paid off handsomely in helping the region weather the cutoff of Russian gas supply through the Yamal pipeline. The Baltic pipe, connecting Norway to Poland through Denmark, began operation in October 2022. A pipeline connection between Lithuania and Poland began operating in May 2022. The Balticconnector connected Finland to the EU gas network for the first time in January 2020, through Estonia.

Altogether, these projects allow pipeline gas from Norway—and LNG entering the EU in Poland, Finland, and Lithuania—to flow throughout the region. Additionally, Latvia has a large underground gas storage facility, adding to the region’s energy security.

Figure 8

Figure 9

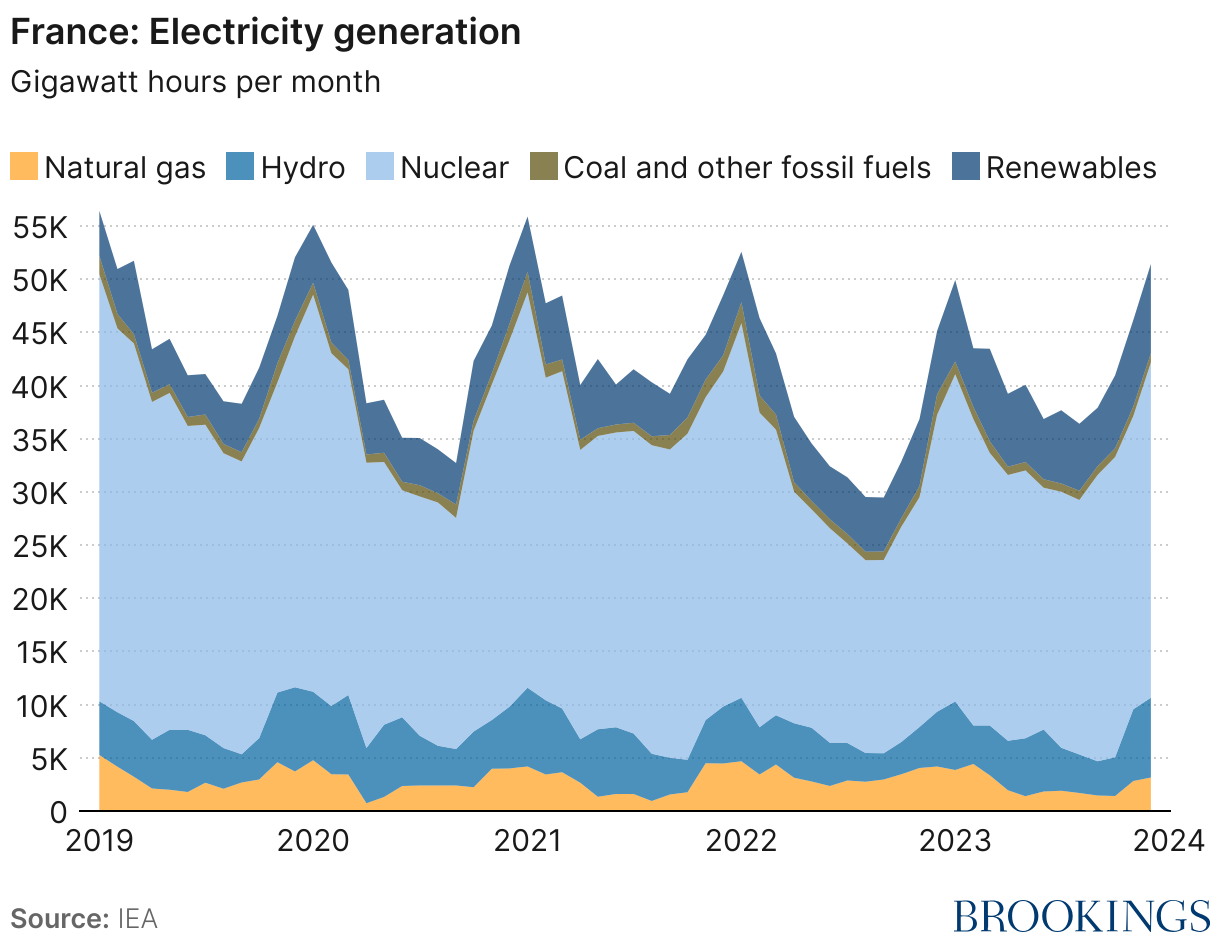

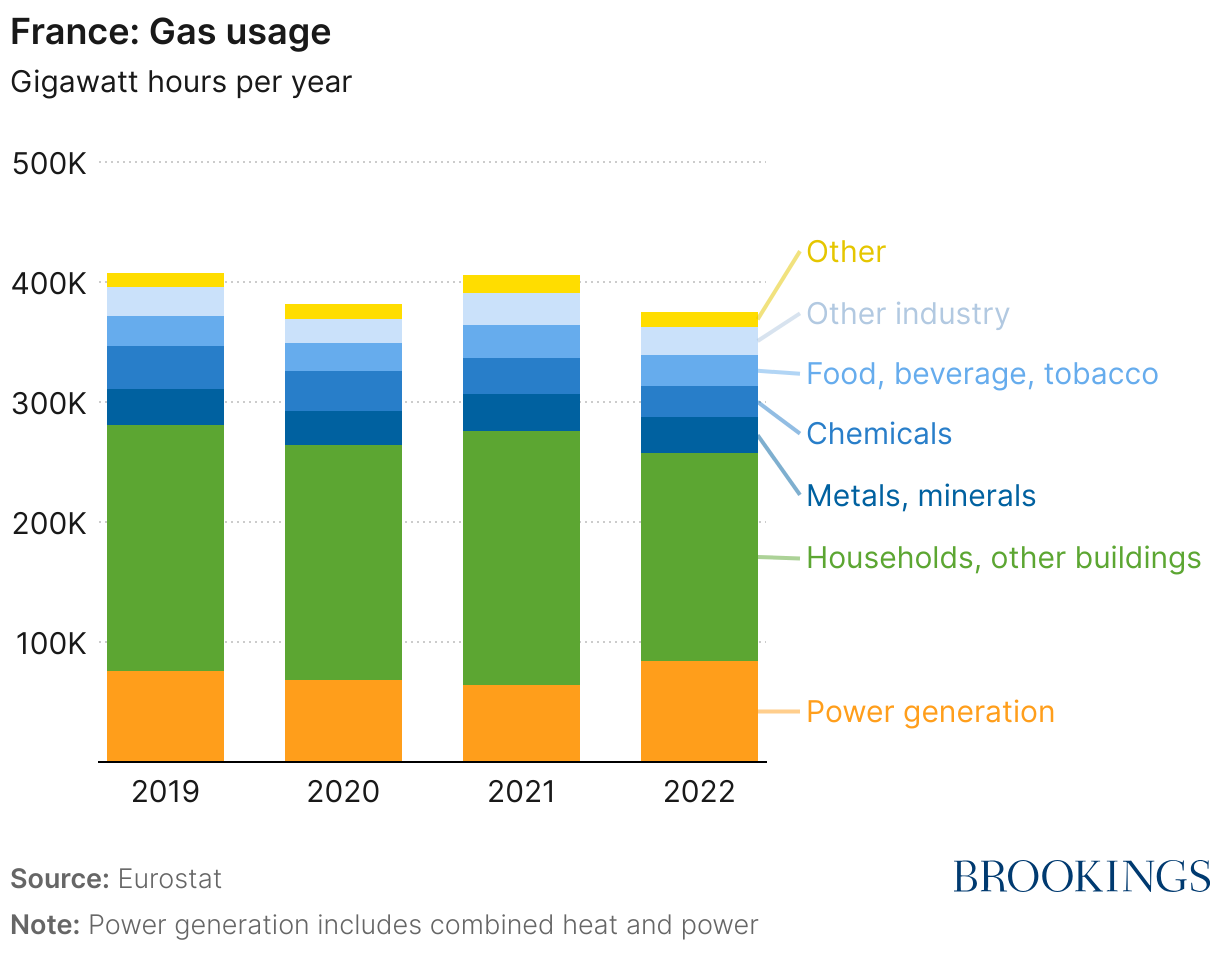

Northwestern connectors: Netherlands, France, Belgium

The Netherlands is unusual in the EU in that it has enjoyed significant domestic natural gas production of its own. The Groningen gas field is the largest in continental Europe, and among the largest in the world. Production began in 1963, but in recent years, production from the field began to cause subsidence and earthquakes. A particularly strong 3.6 magnitude quake in 2012 changed public opinion on gas production and the Dutch government began to limit production from the field. Gas production ended at the field on October 1, 2023, extended one year from the earlier target date because of the crisis.

Because of its history of gas production, the Netherlands also has significant natural gas infrastructure. The Title Transfer Facility (TTF) in the Netherlands is a virtual hub for natural gas trading and is the largest gas trading point in Europe. The TTF is a liquid market that provides pricing for physical contracts and a price curve up to 13 years in the future.

France, the Netherlands, and Belgium are the first, third, and fourth largest LNG importers in the EU, respectively, and are connected to surrounding countries via pipeline networks. These networks are an important part of the new west-to-east flow pattern aimed to replace Russian pipeline gas. Nevertheless, they import significant volumes of Russian LNG, mostly under long-term contracts signed before 2022. France is the largest buyer of Russian LNG in the EU, in part because of the French company TotalEnergies partial ownership stake in the Russian Yamal LNG project. Yamal LNG also has relationships with LNG facilities in France and Belgium to facilitate logistically complicated exports during the Arctic winter.

Figure 10

Figure 11

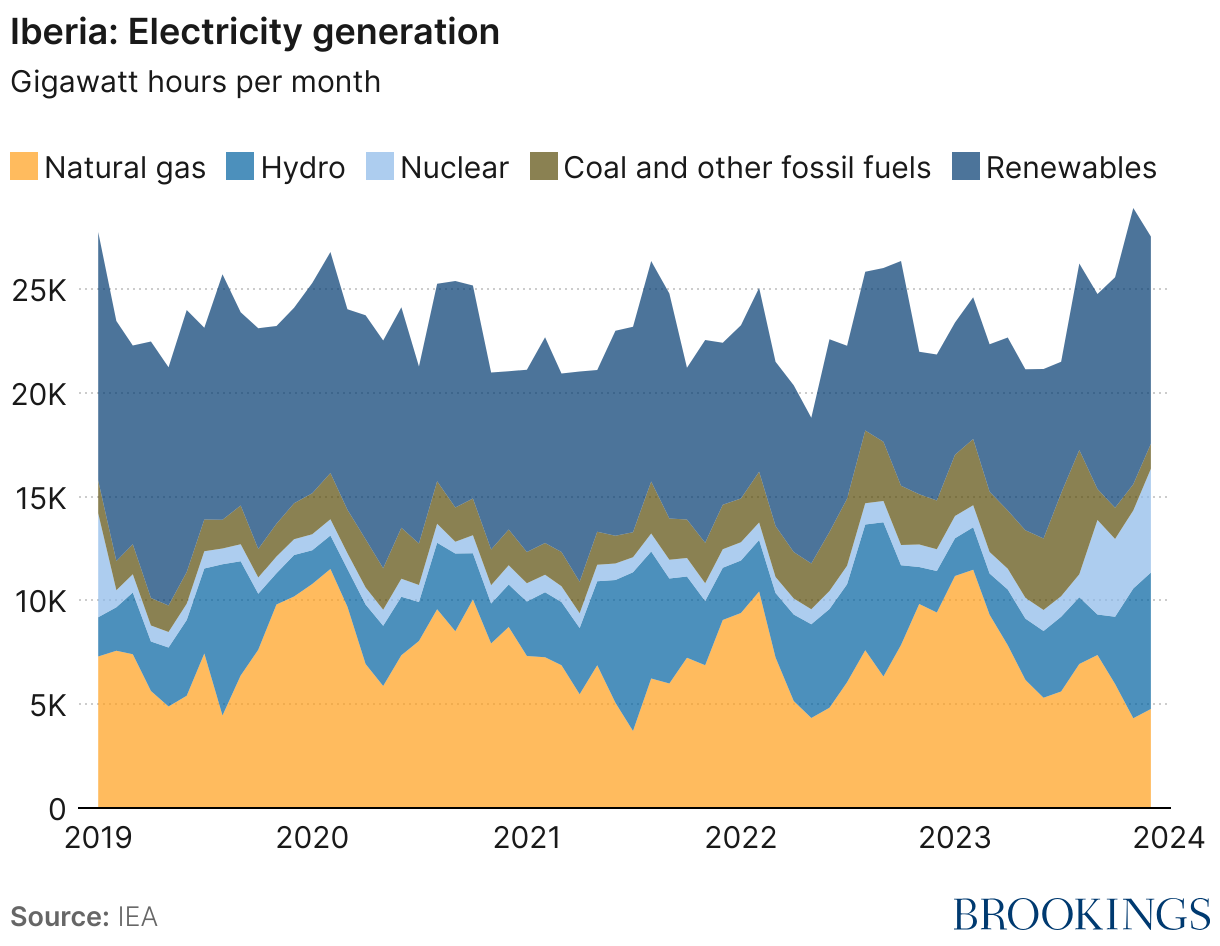

Southwestern connectors: Iberian peninsula

The Iberian Peninsula did not receive Russian pipeline gas, instead relying on LNG imports and pipeline supply from Algeria. Spain has the largest fleet of LNG terminals in Europe, with six facilities in operation and a seventh recently returned to service for storage and logistical purposes. Portugal has one additional terminal. Utilization of these facilities has often been quite low, with an average of 21% utilization between 2012 and 2019 and 36% in 2019. Utilization of Spain’s terminals rose to 40% in 2022.

The Pyrenees Mountains make it difficult to connect the Iberian Peninsula with France, and then the rest of Europe. Two pipelines carry gas between Spain and France. A third pipeline is half-built, but objections from France have prevented the project’s completion. France says the pipeline contravenes climate goals; but, as the Economist observed, “cynics suggest its real aim is to protect its nuclear-power industry.” Gas has flowed both ways on the existing pipelines, with Spain providing gas to France in 2022 while France’s aging and closure-prone nuclear fleet was running below 50% capacity.

An additional challenge to the Iberian gas supply was the shutdown of the Maghreb-Europe gas pipeline from Algeria through Morocco in November 2021. Gas supply was caught in a dispute between Morocco and Algeria over the administration of the Western Sahara. The newer Madgaz pipeline continued to carry Algerian gas, but the Maghreb-Europe pipeline was reversed in June 2022 to carry gas imported into Spain as LNG back to Morocco. This dispute received scant attention amid the larger Russian gas dispute, but also had little implication for supply in greater Europe.

Figure 12

Figure 13

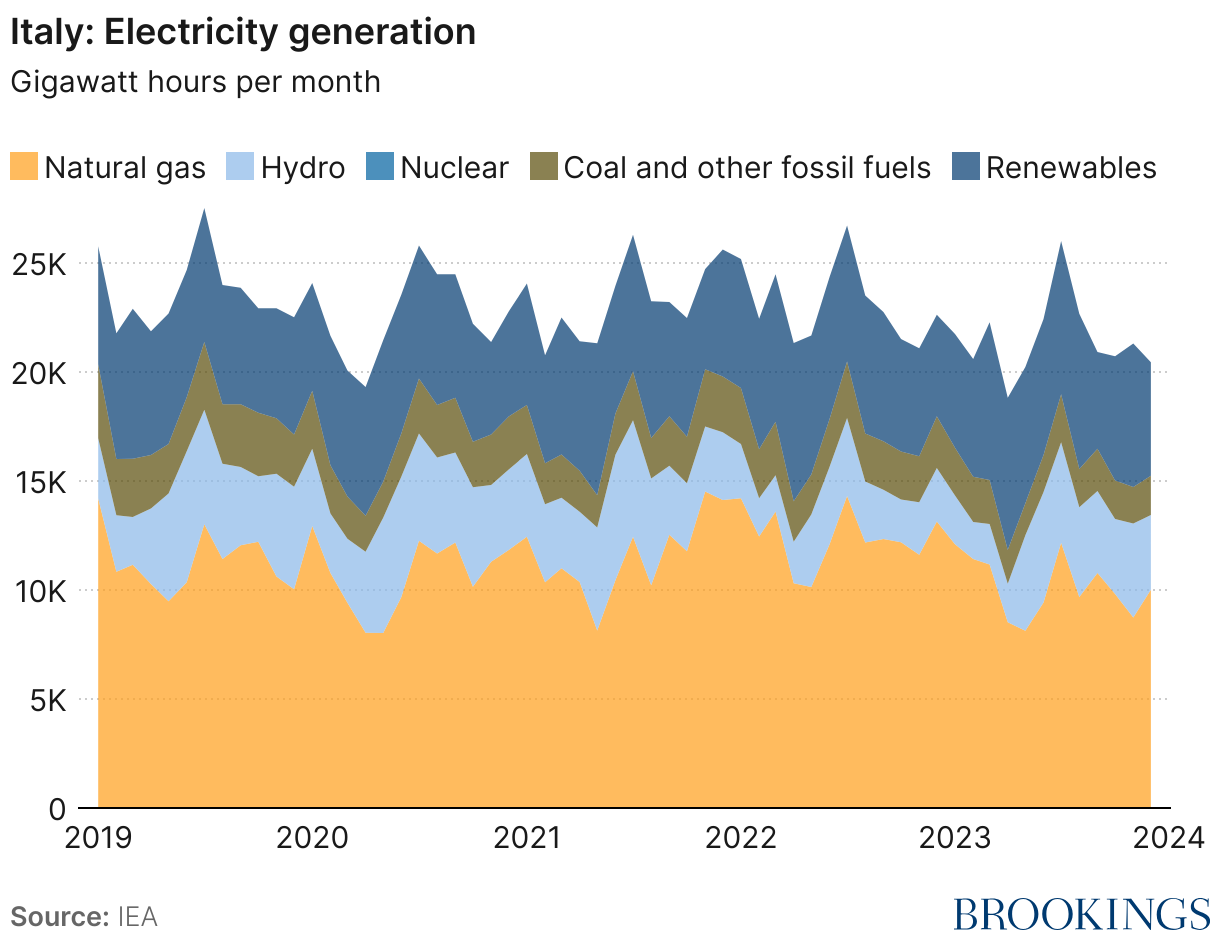

Southeastern connectors: Italy, Greece, Turkey

Before the war, Russia supplied about 40% of Italy’s gas, primarily shipped via pipeline through Ukraine. Italy also receives substantial gas from Algeria and Libya via pipeline. Italy added a FSRU to its LNG import facilities in May 2023 and a second FSRU is planned to begin operation in early 2025. In October 2023, ENI signed a deal to purchase up to 1 million tonnes of LNG annually (or 1.5 bcm) from QatarEnergy for the next 27 years. Italy plans to stop importing Russian natural gas by the second half of 2024.

Natural gas is particularly important in electricity generation in Italy. It accounted for just over half of generation in 2022, the highest share in any of Europe’s large economies. The high share of natural gas generation means that Italy has had the highest power prices in major European markets for the past three years, one-third higher than Germany and France and 50% higher than Spain. Solar and wind generation capacity expanded by 11% and 5% respectively in 2022, but still have a long way to go to replace the dominant share of gas.

Figure 14

Figure 15

Greece was similarly dependent on Russian gas before the war, receiving about 40% of its supply through the TurkStream pipeline. Greece also imported about one-third of its gas supply in 2021 as LNG. In response to the conflict in Ukraine, Greece greatly increased the use of its existing LNG terminal and added an FSRU that began operation in February 2024.

Greece and Italy are also at the center of developments of natural gas supply in the Eastern Mediterranean, with large discoveries in the waters around Israel, Egypt, and Cyprus. Currently, much of this gas is used locally in Israel, Egypt, and their neighbors, and turned into LNG at a facility in Egypt. A proposed pipeline connecting Eastern Mediterranean gas to Greece, Italy, and central Europe is on the European Commission’s list of Projects of Common Interest, meaning that it has access to fast-track permitting processes and special funding. However, the pipeline faces serious challenges due to disputed territory and maritime boundaries in Cyprus. Discussions of the pipeline have been going on for 15 years, and it has been on the European Commission’s favored project list since 2013.

Turkey is an important gas player in southern Europe. It receives gas from Russia and Azerbaijan and sends it to European countries including Bulgaria, Serbia, and Hungary. Russian gas from the TurkStream pipeline can also flow to Romania, Greece, North Macedonia, and Bosnia and Herzegovina. In April 2024 Hungary signed a deal with Turkey to receive gas supply, likely from Russia, to replace the gas that might be lost if Ukraine’s gas transit ends.

End of Ukraine gas transit would decrease Russian gas supply

Despite the war, Russia continues to supply gas to Europe through pipelines that run through Ukraine, although the volume of gas delivered via this route in 2023 (12 bcm) can be calculated as only one-third of the volume delivered in 2021. Prior to the completion of the Nord Stream 1 pipeline, Russia sent more than 110 bcm of gas through Ukraine in some years. The five-year agreement governing this transit expires at the end of 2024 and Kyiv has already announced that it will not extend the agreement.

Natural gas provided via this route enters the EU in Slovakia and is used in Slovakia, Hungary, Austria, and Italy. Italy has many options for supply and Austria is linked to LNG and pipeline gas through Germany. But Slovakia will go from being front of the line, in a geographic sense, for gas from Ukraine to the back of the line for gas delivered from elsewhere. While EU energy commissioner Kadri Simson has said that the transit gas recipients will be able to substitute, Slovakia’s pro-Russian prime minister Robert Fico has called on Ukraine to extend the transit agreement.

There are also questions about whether it is in Ukraine’s interest to stop gas transport from Russia. When the Ukrainian economy begins to grow again and its domestic gas production is insufficient to meet demand, Ukraine will incur significant costs to obtain gas supply from elsewhere in Europe. Additionally, EU countries use gas storage facilities (the second largest on the continent after Russia at nearly 33 bcm) in western Ukraine, but don’t actually transport gas to these facilities. Instead, they “swap” gas at EU facilities for Russian gas held in Ukraine to be used later. These transactions would not be possible without Russian gas supply. Russia too might have good reasons to change its mind about extending the gas transport deal, since the gas it supplies via this route has no other path to market.

Future US LNG supply and the 2024 elections

Immediately after the Russian invasion, the Biden administration and the EU created a U.S.-EU Task Force on Energy Security, with the U.S. promising to deliver at least 15 bcm of additional LNG in 2022, with likely larger increases to follow, and the EU pledging to ensure stable demand of at least 50 bcm per year until 2030. European LNG imports from the U.S. have in fact more than doubled between 2.6 bcm in December 2021 and 5.9 bcm in April 2024—more than half of all of the EU’s LNG imports. In other words: the outcome of the 2024 American elections is meaningful for Europe’s energy security.

The Biden administration celebrated its LNG deliveries as a crucial contribution to the security of its allies. Then, in January 2024, U.S. President Joe Biden announced a pause in approvals of new LNG exports to countries without free trade agreements with the United States (including the EU). The pause is intended to allow time to reconsider the climate, environmental, and economic impacts of additional LNG exports. Yet it does not affect projects that are already under construction or past the final investment decision, all of which will bring a doubling of US LNG export capacity by 2030. Meanwhile, given the speed with which European gas users are working to move toward zero-carbon sources of energy, European LNG importers have been reluctant to sign long-term contracts. But new U.S. LNG projects will require contract commitments—likely a greater impediment to growing future supply than the LNG pause.

Neither the Republican candidate for U.S. president, Donald Trump, nor the Republican Party has released a platform in advance of the U.S. elections in November 2024. However, the conservative Heritage Foundation led an effort called Project 2025, designed to provide a ready-to-go policy agenda for the next Republican administration.

The energy portion in chapter 12 of this document emphasizes U.S. fossil fuel production and specifically states that the next conservative administration should focus on “promoting U.S. energy resources as a means to assist our allies, diminish our strategic adversaries, and ensure the existence of markets that will support domestic energy production.” Additionally, the document calls on Congress to reform the Natural Gas Act to expand required LNG project approvals to all of America’s allies, specifically referring to NATO, instead of only nations with free trade agreements, as in the current applicable law. These words sound like good news for European LNG importers. But the Republican candidate’s repeated expressions of disdain for NATO, Europe, and Ukraine suggest European allies ought to be cautious about presuming on U.S. supply security, should the next U.S. president be a Republican.

Resilience and its price

In retrospect, it is clear that the Kremlin’s preparations for the weaponization of Europe’s dependency on Russian oil and gas began well before the full-scale invasion of Ukraine, in the form of slowed-down supplies and near-empty storage facilities. After February 24, 2022, when Russia completely shut down its two major gas pipelines to Germany and Central Europe, its actions created a massive supply and price shock that reverberated across the continent and could well have led to widespread socio-economic upheavals and political paralysis.

Yet Europe’s overall reaction has been (with the help of some remarkable luck) surprisingly resilient. While the G-7 price cap on Russian oil has had mixed results, Europeans were able to wean themselves off Russian gas almost completely through demand reduction and substitution with LNG, leading to what Alexandra Gritz and Guntram Wolff of the German Council on Foreign Relations call a “massive adaptation of the energy system.” As the Cambridge economist Helen Thompson drily notes, “gas dependency has not proved to be the weapon Putin envisaged during the mid-2010s…for Russia, Europe’s resilience has been a geopolitical disaster, since unlike with oil, Gazprom cannot replace European customers with Asian ones.” Natural gas prices are back to pre-crisis levels.

Yet as this paper shows, the trajectory of decoupling and adaptation has been quite different from one country to the next; and it has come at a high price: severe hits to energy-intensive industries, controversial subsidies and beggar-thy-neighbor policies, and heightened political tensions within and between European countries. Above all, it is incomplete and vulnerable to future shocks, such as continued blackmail against the remaining European importers of Russian gas, the end of the Ukrainian gas transit agreement, an unfavorable election outcome in the United States, or the high political and price volatility that is typical for the LNG market. In sum, Europe for now remains largely dependent on imported gas; it has just diversified its suppliers and increased its relative dependence on more expensive LNG. Maintaining European industrial competitiveness given high LNG prices and immense government subsidy schemes for clean energy in the United States and China will be a challenge. Energy autarky is of course unattainable for Europe. But the experience of 2022-2024 should be a powerful driver for strengthening supply security, assuring cross-border flows, and investing in renewables and the green energy transition.

Finally, key policy questions still need to be addressed: what should the relative roles of markets and governments be in managing the gas economy and allocating scarce resources? If gas supply security is now part of the security posture of an interdependent, open, and globalized continent, what does that mean for the status of critical infrastructure and energy companies? What role should the European Union play in integrating the European gas market, and in addressing inequalities of distribution and beggar-thy-neighbor fiscal policy responses? And finally, how does all this play into the trans-Atlantic alliance—should energy security be part of NATO’s remit, and if so, in what form? Future papers in this series will address these questions and more.

Acknowledgements

The authors would like to thank Louison Sall and Sophie Roehse for their research support, Rachel Slattery for layout and graphics, as well as Adam Lammon, Alexandra Dimsdale, and Ted Reinert for editing.